Understanding your financial position compared to others can be one of the most powerful ways to evaluate long-term wealth growth. That is why the topic “net worth percentile by age” has become increasingly popular among people interested in personal finance, retirement planning, investments, and wealth management. Whether you are in your 20s trying to build savings or in your 50s preparing for retirement, comparing your net worth to others in your age group can provide valuable insight into your financial progress.

Net worth percentile by age measures how your total wealth compares with people of a similar age range. It includes assets such as cash savings, investments, retirement accounts, real estate, businesses, and valuable possessions minus debts like mortgages, student loans, and credit card balances. By understanding these percentiles, individuals can identify whether they are ahead, average, or behind financially.

In 2026, rising inflation, changing investment markets, and increasing living costs have made financial planning more important than ever. Many people are now focusing on building long-term wealth through investing, side businesses, retirement savings, and property ownership. This guide explores net worth percentiles across different age groups, explains how wealth grows over time, highlights income strategies, and provides realistic financial benchmarks to help readers understand their current financial standing.

Net worth figures and percentile estimates are based on publicly available financial data, household wealth surveys, investment trends, and economic research. Actual financial situations may vary depending on income, location, debt, lifestyle, and investment performance.

Bio Data Table

| Category | Details |

|---|---|

| Topic | Net Worth Percentile by Age |

| Main Focus | Personal Finance & Wealth Comparison |

| Search Intent | Informational & Financial Analysis |

| Primary Audience | Investors, Professionals, Young Adults, Retirees |

| Financial Metric | Net Worth |

| Includes | Assets, Savings, Investments, Debt |

| Wealth Factors | Income, Real Estate, Retirement Funds |

| Common Assets | Cash, Stocks, Property, Businesses |

| Common Liabilities | Loans, Mortgages, Credit Card Debt |

| Best Use | Retirement Planning & Wealth Tracking |

| Financial Goal | Long-Term Wealth Growth |

| Relevant Age Groups | 20s, 30s, 40s, 50s, 60s |

| Key Wealth Drivers | Investing, Saving, Income Growth |

| Financial Benchmarks | Percentile Rankings |

| Economic Influence | Inflation, Markets, Interest Rates |

| Wealth Strategy | Diversification & Compound Growth |

| Risk Factors | Debt, Poor Spending Habits |

| Long-Term Objective | Financial Independence |

What Is Net Worth Percentile by Age?

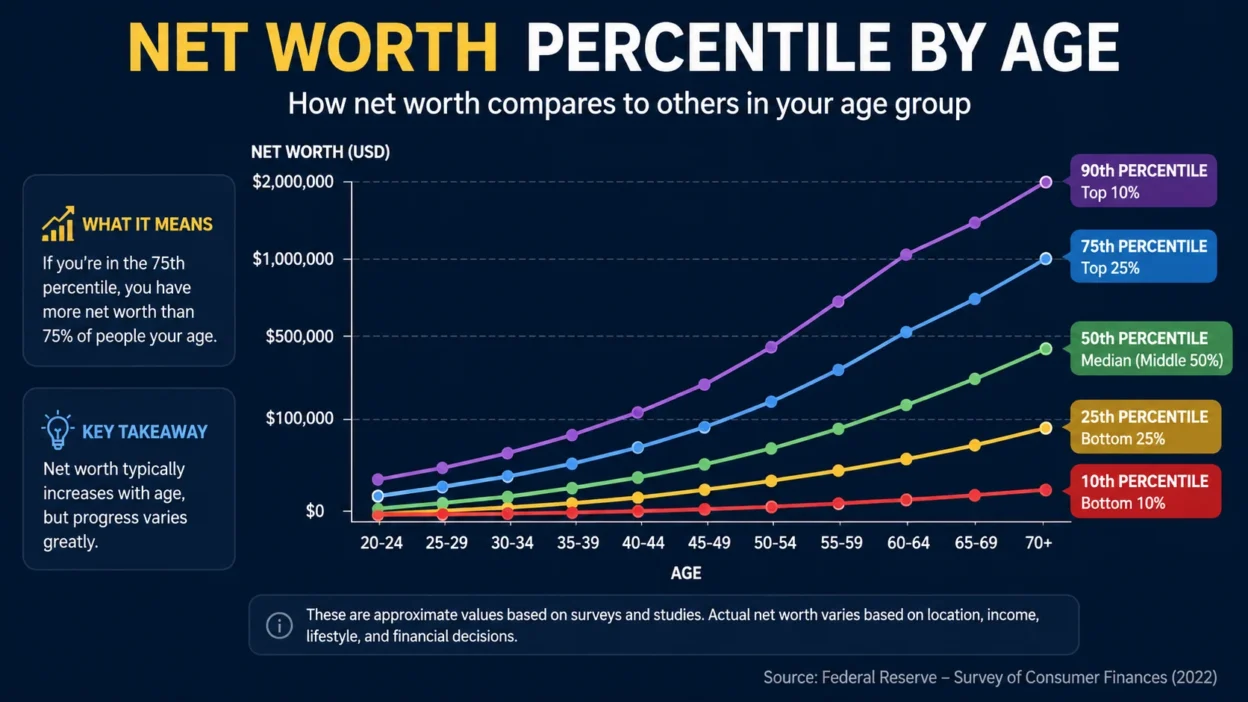

Net worth percentile by age refers to how your total wealth compares with others in your age group. A percentile ranking helps determine your financial position relative to the broader population. For example, if your net worth places you in the 80th percentile for your age, it means you have more wealth than 80% of people in the same age category.

Net worth itself is calculated by subtracting liabilities from total assets. Assets include checking accounts, savings accounts, retirement funds, investments, businesses, and real estate. Liabilities include mortgages, student loans, car loans, personal loans, and credit card debt.

Understanding percentiles can help individuals evaluate whether they are meeting financial milestones. It also provides perspective because financial growth naturally changes with age. Younger adults generally have lower net worth due to education costs and early career stages, while older individuals often benefit from decades of compound investing, property appreciation, and retirement savings.

Percentiles are not designed to create unhealthy competition. Instead, they act as benchmarks to encourage smarter money decisions and long-term planning.

Net Worth Overview in 2026

In 2026, wealth inequality continues to shape net worth distribution across age groups. Rising home prices, stock market growth, and retirement investment gains have increased wealth for many households, while inflation and debt continue to challenge others.

Average net worth often appears significantly higher because wealthy households heavily influence the data. Median net worth is generally considered a more accurate representation because it reflects the midpoint of financial distribution.

The following table provides estimated net worth percentiles by age in the United States for 2026.

Net Worth Percentile by Age Table

| Age Group | Median Net Worth | Top 25% | Top 10% | Top 1% |

|---|---|---|---|---|

| Under 25 | $15,000 | $75,000 | $200,000 | $1 Million |

| 25–34 | $85,000 | $300,000 | $850,000 | $5 Million |

| 35–44 | $220,000 | $750,000 | $2 Million | $10 Million |

| 45–54 | $450,000 | $1.5 Million | $4 Million | $20 Million |

| 55–64 | $700,000 | $2.5 Million | $6 Million | $30 Million |

| 65+ | $600,000 | $2 Million | $5 Million | $25 Million |

These figures vary depending on geographic location, market performance, and income levels. High-cost cities often produce higher asset values due to real estate appreciation.

Net Worth Growth Timeline

Early Adulthood (20s)

Most individuals in their 20s begin building financial foundations through employment, education, and savings. Student loans often reduce net worth during this stage, but consistent investing and budgeting can create strong long-term growth.

The biggest advantage in this age group is time. Even small investments can grow significantly through compound interest over several decades.

Career Building Years (30s)

In the 30s, income generally increases as careers advance. Many people purchase homes, build retirement accounts, and start families during this stage. Net worth often grows rapidly because earnings rise while investments continue compounding.

Those who invest consistently in stocks, retirement plans, and property tend to move into higher wealth percentiles.

Peak Earning Years (40s and 50s)

The 40s and 50s are usually the strongest wealth-building decades. Individuals often reach senior career positions, expand investments, and pay down debt.

Real estate equity, retirement savings, business ownership, and diversified portfolios significantly increase total assets during this period.

Retirement Stage (60s and Beyond)

In retirement years, financial priorities shift toward wealth preservation and passive income. Many retirees rely on pensions, investment returns, Social Security, and rental income.

Net worth may decline slightly due to spending in retirement, but strong investment planning can maintain financial stability for decades.

Main Sources of Wealth Growth

Employment and Salary Income

For most households, earned income remains the largest driver of wealth accumulation. Higher salaries increase the ability to save, invest, and purchase appreciating assets.

Professionals in technology, medicine, finance, law, and entrepreneurship often achieve higher net worth percentiles due to elevated income potential.

Investments and Compound Growth

Investments play a major role in long-term wealth building. Stock market investments, retirement accounts, index funds, and dividend portfolios generate compound returns over time.

Individuals who begin investing early often reach higher net worth percentiles because compound growth accelerates over decades.

Real Estate Ownership

Homeownership remains one of the strongest wealth-building tools. Rising property values increase equity and improve overall net worth.

Rental properties can also generate passive income while appreciating in value.

Business Ownership

Entrepreneurship significantly impacts wealth percentiles. Many high-net-worth individuals own businesses that generate long-term income and asset growth.

Business equity often becomes one of the largest components of total net worth.

Retirement Accounts

401(k) plans, IRAs, pensions, and retirement investment accounts create financial security later in life.

Consistent contributions over time help individuals move into higher wealth percentiles.

Business Strategy Behind Wealth Building

People who achieve higher net worth percentiles usually follow disciplined financial strategies. They prioritize saving, investing, minimizing unnecessary debt, and diversifying income streams.

One of the most effective wealth-building strategies is living below one’s means. High-income individuals who spend carefully often accumulate more wealth than those with expensive lifestyles.

Another important strategy is diversification. Wealthy households commonly hold multiple asset types including stocks, real estate, retirement funds, and businesses.

Long-term thinking also matters. Building wealth is typically a gradual process rather than a quick financial success story.

Financial Milestones by Age

In Your 20s

- Build emergency savings

- Eliminate high-interest debt

- Begin retirement investing

- Develop budgeting habits

- Improve income skills

In Your 30s

- Increase investment contributions

- Purchase property if possible

- Build multiple income streams

- Grow retirement accounts

- Protect assets with insurance

Your 40s

- Maximize retirement savings

- Reduce debt aggressively

- Diversify investments

- Increase passive income

- Focus on wealth preservation

In Your 50s and Beyond

- Prepare retirement strategy

- Shift toward stable investments

- Reduce financial risks

- Maintain healthcare planning

- Create estate plans

Assets and Lifestyle Impact on Net Worth

Real Estate Assets

Property ownership heavily influences wealth rankings. Individuals in higher percentiles often own multiple properties or homes in appreciating markets.

Mortgage reduction also improves net worth over time because liabilities decrease while property values may increase.

Cars and Luxury Spending

Luxury spending can either support or damage wealth growth depending on financial discipline.

Many high-net-worth individuals avoid excessive spending on depreciating assets such as luxury cars.

Investments and Ownership

Ownership remains one of the most powerful wealth-building tools. Stocks, businesses, and real estate create long-term appreciation while generating passive income.

Individuals focused on ownership generally outperform those relying solely on earned income.

Net Worth Comparison Across Income Groups

Households in higher income brackets generally achieve stronger net worth percentiles because they can invest larger amounts consistently.

However, income alone does not guarantee wealth. Spending habits, debt management, and investment behavior often matter more over the long term.

Some moderate-income households build impressive net worth through disciplined investing and low living costs.

Challenges and Financial Risks

Inflation

Inflation reduces purchasing power and can slow wealth accumulation if income growth fails to keep pace.

Debt

High-interest debt is one of the biggest barriers to building net worth. Credit card balances and personal loans reduce financial flexibility.

Market Volatility

Stock market declines and real estate downturns can temporarily reduce net worth.

Long-term investing strategies generally help overcome short-term volatility.

Lifestyle Inflation

As income increases, many people increase spending dramatically. This prevents wealth accumulation despite higher salaries.

Financial Habits of High-Net-Worth Individuals

People in top net worth percentiles often share similar habits:

- Consistent investing

- Long-term financial planning

- Multiple income streams

- Strong budgeting discipline

- Continuous skill development

- Focus on asset ownership

- Low unnecessary debt

These habits create compounding financial advantages over time.

How People Increase Net Worth Outside Traditional Jobs

Many individuals build wealth outside standard employment through side businesses, investing, freelancing, content creation, consulting, and digital entrepreneurship.

Passive income strategies such as rental properties, dividends, royalties, and online businesses also contribute significantly to wealth growth.

Technology and remote work opportunities have expanded the number of ways individuals can improve their net worth percentiles.

Future Wealth Trends

Future net worth trends are likely to be shaped by artificial intelligence, digital assets, remote work, entrepreneurship, and investment technology.

Financial education is becoming increasingly accessible, allowing younger generations to start investing earlier than previous generations.

At the same time, rising housing costs and economic uncertainty may continue creating wealth gaps between income groups.

People who focus on adaptability, skill development, and long-term investing are likely to achieve stronger financial outcomes over the next decade.

Frequently Asked Questions

What is considered a good net worth by age?

A good net worth depends on income, location, and financial goals. Generally, being above the median for your age group indicates strong financial progress.

What net worth percentile is considered wealthy?

Individuals in the top 10% or top 1% percentile are generally considered wealthy based on national financial benchmarks.

How is net worth calculated?

Net worth equals total assets minus total liabilities.

Does retirement savings count toward net worth?

Yes, retirement accounts such as 401(k)s and IRAs are included in net worth calculations.

Why is median net worth more important than average net worth?

Median net worth better represents typical households because average figures are heavily influenced by extremely wealthy individuals.

Can young adults achieve high net worth percentiles?

Yes, strong investing habits, entrepreneurship, and high-income careers can help younger individuals reach higher wealth percentiles earlier.

Conclusion

Understanding net worth percentile by age provides valuable insight into personal financial progress and long term wealth potential. Comparing your financial position with age-based benchmarks can help identify strengths, weaknesses, and opportunities for growth. While income matters, true wealth is usually built through disciplined saving, investing, ownership, and smart financial planning.

The most important lesson is that wealth building is a long-term process. Individuals who invest consistently, avoid excessive debt, diversify income streams, and focus on financial education generally improve their net worth steadily over time. Whether someone is just beginning their financial journey or preparing for retirement, understanding net worth percentiles can support better money decisions and stronger financial confidence.