Understanding the median net worth by age is one of the best ways to measure your financial progress and compare your wealth with people in similar stages of life. you’re in your 20s building your first savings account or approaching retirement in your 60s, net worth provides a clear picture of your overall financial health. Unlike income, which only reflects how much money you earn, net worth represents the total value of your assets minus your liabilities.

As of 2026, the median net worth varies significantly across different age groups due to factors such as career growth, investments, homeownership, retirement savings, and debt management. While younger individuals often have lower net worth because they are still paying off student loans or starting their careers, older adults generally accumulate more wealth through decades of saving and investing.

This guide provides a comprehensive breakdown of median net worth by age, explains how wealth changes throughout life, and offers strategies to help you build long-term financial security.

Key Statistics Table: Median Net Worth by Age

| Age Group | Median Net Worth (2026 Estimate) |

|---|---|

| Under 35 | $45,000 |

| 35–44 | $135,000 |

| 45–54 | $265,000 |

| 55–64 | $395,000 |

| 65–74 | $410,000 |

| 75 and Above | $335,000 |

These figures represent the midpoint of household wealth, meaning half of households have a higher net worth and half have a lower net worth.

What Is Net Worth?

Net worth is a financial measurement used to determine a person’s overall wealth. It is calculated by subtracting total liabilities from total assets.

Assets Include:

- Cash and savings

- Checking accounts

- Retirement accounts

- Stocks and mutual funds

- Real estate

- Vehicles

- Businesses

- Valuable possessions

Liabilities Include:

- Credit card debt

- Student loans

- Car loans

- Mortgages

- Personal loans

A positive net worth means your assets exceed your debts, while a negative net worth indicates that liabilities outweigh assets.

Why Median Net Worth Matters More Than Average Net Worth

Many people confuse median net worth with average net worth. Although both measurements describe wealth, the median often provides a more realistic picture.

Average Net Worth

Average net worth is calculated by adding all household wealth together and dividing it by the number of households. Because billionaires and millionaires have extremely high wealth, the average can be skewed upward.

Median Net Worth

Median net worth represents the middle point. Half the population has more wealth, while half has less.

Financial experts generally consider the median a better indicator because it reflects the typical financial position of households rather than being influenced by the wealthiest individuals.

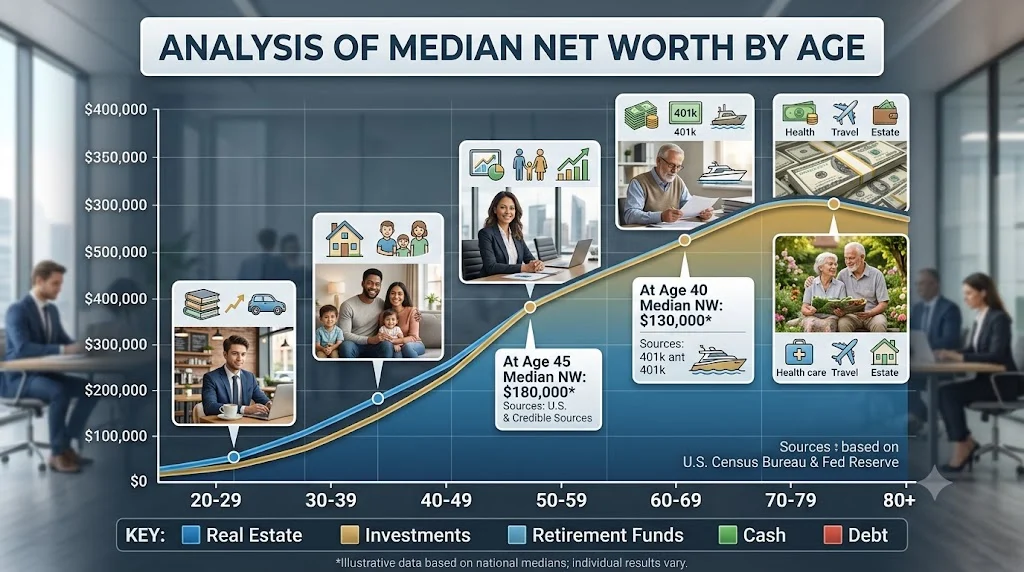

Median Net Worth by Age Group

Under Age 35

People under 35 are often in the early stages of their careers. Many are still paying off student loans, building emergency funds, and saving for major purchases.

Median Net Worth: Approximately $45,000

Common assets include:

- Savings accounts

- Retirement contributions

- Cars

- Small investment portfolios

Major liabilities include:

- Student debt

- Credit card balances

- Auto loans

During this stage, increasing income and avoiding excessive debt are essential for long-term financial growth.

Ages 35–44

By their late 30s and early 40s, many individuals experience higher earnings and begin accumulating substantial assets.

Median Net Worth: Approximately $135,000

Financial characteristics include:

- Home ownership

- Growing retirement accounts

- Family expenses

- Investment portfolios

Many households in this age group prioritize balancing debt repayment with wealth accumulation.

Ages 45–54

Peak earning years often occur during this period. Careers become more established, and retirement savings accelerate.

Median Net Worth: Approximately $265,000

Common wealth-building assets include:

- Equity in homes

- 401(k) accounts

- Stocks and bonds

- Business ownership

Individuals in this stage often focus on maximizing retirement contributions and reducing debt.

Ages 55–64

As retirement approaches, wealth accumulation reaches its highest levels for many households.

Median Net Worth: Approximately $395,000

Assets commonly include:

- Fully funded retirement accounts

- Real estate holdings

- Investment portfolios

- Savings accounts

People in this age range often work toward becoming debt-free before retirement.

Ages 65–74

Retirement begins for many individuals in this group.

Median Net Worth: Approximately $410,000

Financial priorities shift toward:

- Preserving wealth

- Managing withdrawals

- Healthcare planning

- Estate planning

Because expenses often decline after retirement, many households maintain stable net worth levels.

Age 75 and Older

At this stage, wealth may gradually decline as retirement savings are spent.

Median Net Worth: Approximately $335,000

Major financial concerns include:

- Medical expenses

- Long-term care costs

- Estate transfers

- Income preservation

Despite reduced earnings, many seniors maintain significant assets accumulated over decades.

Net Worth Growth Timeline

Early Adulthood (20s)

Most individuals focus on:

- Education

- Career development

- Saving money

- Paying off debt

Net worth growth is typically slow but forms the foundation for future wealth.

Mid-Career Years (30s and 40s)

Income usually increases substantially.

People begin accumulating:

- Home equity

- Retirement funds

- Investment accounts

This stage often produces rapid increases in net worth.

Peak Earning Years (50s)

Many individuals reach their highest salaries during this period.

Major goals include:

- Eliminating debt

- Maximizing retirement savings

- Diversifying investments

Wealth accumulation accelerates significantly.

Retirement Years (60s and Beyond)

Retirees focus more on preserving assets than growing them aggressively.

Financial priorities include:

- Generating passive income

- Managing expenses

- Protecting investments

- Estate planning

Main Sources of Wealth by Age

Income From Employment

Salary remains the largest contributor to net worth during working years.

Higher earnings generally allow individuals to save and invest more effectively.

Home Ownership

Real estate is one of the biggest wealth generators for middle-class households.

As mortgages are paid down and property values increase, home equity contributes significantly to net worth.

Retirement Accounts

401(k)s, IRAs, pensions, and other retirement accounts often represent the largest assets for older households.

Investment Portfolios

Stocks, bonds, ETFs, and mutual funds provide long-term growth and compound returns.

Business Ownership

Entrepreneurs frequently accumulate wealth faster than wage earners due to business equity.

Factors That Influence Net Worth

Several factors determine how much wealth individuals accumulate over time.

Education

Higher education often leads to increased earning potential.

Career Choice

Professions with higher salaries generally support faster wealth accumulation.

Spending Habits

People who control expenses and save consistently tend to build greater wealth.

Investment Strategy

Long-term investing helps compound returns and increase assets.

Debt Management

Reducing liabilities improves overall net worth and financial flexibility.

How to Increase Your Net Worth

Improving net worth does not happen overnight. Consistent financial habits are essential.

Build an Emergency Fund

Having three to six months of expenses saved protects against unexpected setbacks.

Invest Early

Compound interest rewards those who start investing at a young age.

Eliminate High-Interest Debt

Paying off credit card balances can dramatically improve financial health.

Increase Income

Additional income streams can accelerate wealth accumulation.

Save for Retirement

Regular contributions to retirement accounts provide tax advantages and long-term growth.

Investment Strategies for Building Wealth

Investing is one of the most effective ways to increase net worth over time. While saving money is important, investing allows individuals to benefit from compound growth and potentially outpace inflation. Different age groups often adopt different investment strategies based on their financial goals and risk tolerance.

Investing in Your 20s and 30s

Young investors typically have the advantage of time. Because retirement is decades away, they can afford to take more risks and focus on long-term growth.

Common investment options include:

- Index funds

- Exchange-traded funds (ETFs)

- Individual stocks

- Retirement accounts

- High-yield savings accounts

Starting early gives investments more time to compound, which can dramatically increase wealth over several decades.

Investing in Your 40s and 50s

During peak earning years, many individuals focus on balancing growth and security. Portfolios often become more diversified to protect accumulated wealth.

Popular investments include:

- Mutual funds

- Dividend-paying stocks

- Bonds

- Real estate

- Retirement plans

At this stage, increasing retirement contributions becomes a top priority.

Investing After Age 60

Retirees and near-retirees generally prioritize income and capital preservation. While growth remains important, reducing risk becomes equally essential.

Common choices include:

- Bonds

- Dividend stocks

- Certificates of deposit (CDs)

- Income-producing real estate

- Annuities

The goal shifts from aggressive growth to maintaining financial stability and generating reliable income.

Wealth-Building Habits of High-Net-Worth Individuals

Many financially successful people share similar habits that help them accumulate wealth over time.

Living Below Their Means

One of the most important principles of wealth creation is spending less than you earn. High-net-worth individuals often avoid lifestyle inflation and prioritize saving.

Consistent Investing

Regular investments, even in small amounts, can lead to significant wealth through compound growth.

Diversification

Successful investors rarely depend on one asset class. They spread their investments across:

- Stocks

- Bonds

- Real estate

- Businesses

- Retirement accounts

Diversification helps reduce risk and improve long-term returns.

Avoiding Excessive Debt

Managing liabilities effectively allows more money to be directed toward investments and savings.

Setting Financial Goals

People with clear financial objectives are often more disciplined and successful in building wealth.

Average Net Worth vs. Median Net Worth by Age

Many people wonder why average net worth figures are often much higher than median figures.

Under Age 35

- Average Net Worth: Approximately $180,000

- Median Net Worth: Approximately $45,000

- Ages 35–44

- Average Net Worth: Approximately $550,000

- Median Net Worth: Approximately $135,000

- Ages 45–54

- Average Net Worth: Approximately $975,000

- Median Net Worth: Approximately $265,000

- Ages 55–64

- Average Net Worth: Approximately $1.4 Million

- Median Net Worth: Approximately $395,000

The large difference occurs because extremely wealthy households raise the average significantly. Median figures provide a clearer picture of the typical household’s financial position.

Common Financial Mistakes That Reduce Net Worth

Building wealth requires avoiding mistakes that can slow progress.

Carrying High-Interest Debt

Credit card debt is one of the biggest obstacles to financial success. High interest rates make it difficult to accumulate wealth.

Delaying Investments

Waiting too long to invest reduces the benefits of compound growth.

Lack of Emergency Savings

Unexpected expenses can force people into debt if they lack adequate savings.

Overspending

Lifestyle inflation often prevents higher earners from increasing their net worth.

Ignoring Retirement Planning

Failing to save consistently for retirement can create financial challenges later in life.

How Home Ownership Affects Net Worth

For many households, home equity represents the largest asset.

Benefits of owning a home include:

- Appreciation in property value

- Forced savings through mortgage payments

- Tax advantages

- Long-term wealth accumulation

However, homeownership also involves costs such as:

- Property taxes

- Maintenance expenses

- Insurance

- Mortgage interest

Although real estate can significantly increase net worth, it should be viewed as part of a diversified financial strategy.

Retirement Planning and Net Worth

Retirement planning plays a critical role in long-term wealth accumulation.

Employer Retirement Plans

Accounts such as 401(k)s offer tax advantages and employer matching contributions.

Individual Retirement Accounts (IRAs)

IRAs provide additional opportunities to save for retirement while benefiting from tax advantages.

Social Security Benefits

Although Social Security provides income during retirement, experts generally recommend supplementing it with personal savings and investments.

Healthcare Planning

Medical expenses often increase with age, making healthcare planning an essential component of retirement preparation.

Wealth Benchmarks by Age

While everyone’s financial journey is different, the following benchmarks provide general guidelines.

By Age 30

A positive net worth and emergency savings are important milestones.

By Age 40

Many experts recommend having approximately three times your annual salary saved for retirement.

By Age 50

Six times annual income saved for retirement is often considered a strong benchmark.

By Age 60

Individuals should ideally have eight to ten times their annual income invested for retirement.

These benchmarks are not strict rules but can help individuals evaluate their financial progress.

How Inflation Impacts Net Worth

Inflation reduces purchasing power over time. Even if assets remain unchanged, rising prices can effectively lower real wealth.

Strategies for combating inflation include:

- Investing in stocks

- Owning real estate

- Maintaining diversified portfolios

- Increasing income streams

Long-term investments historically have provided returns that outpace inflation.

Future Trends in Wealth Building

Several trends are expected to influence median net worth by age in the coming years.

Increased Digital Investing

Online brokerage platforms have made investing more accessible than ever.

Growth of Passive Income

People increasingly seek additional income through:

- Dividend investing

- Rental properties

- Online businesses

- Side hustles

Longer Lifespans

Longer life expectancy requires larger retirement savings and more careful financial planning.

Technological Advancements

Technology continues to create new investment opportunities and income streams.

Frequently Asked Questions

What is the median net worth by age in 2026?

Median net worth varies by age group, ranging from approximately $45,000 for individuals under 35 to around $410,000 for those aged 65–74.

Why is median net worth more important than average net worth?

Median net worth provides a more accurate picture of typical household wealth because it is not heavily influenced by extremely wealthy individuals.

What should my net worth be at age 40?

There is no universal number, but many financial experts recommend building retirement savings equal to roughly three times your annual income by age 40.

How can I increase my net worth?

Increasing income, investing consistently, reducing debt, and controlling spending are effective ways to improve net worth.

Does owning a home increase net worth?

Yes. Home equity often represents a significant portion of household wealth and contributes positively to net worth.

Can someone have a negative net worth?

Yes. If liabilities exceed assets, a person has a negative net worth. This situation is common among young adults with student loans or large debts.

Conclusion

Understanding the median net worth by age provides valuable insight into financial progress and long-term wealth building. Although net worth varies considerably depending on age, income, and lifestyle choices, consistent saving, investing, and debt management remain the keys to financial success. Whether you’re just beginning your career or preparing for retirement, focusing on increasing assets and minimizing liabilities can help you achieve greater financial security. Rather than comparing yourself to others, use median net worth benchmarks as a guide and continue making decisions that support your long-term goals.

Discover More Post

310+ Opossum Puns and Jokes For 2025 – Punified.com –

ABA Puns So Good They Reinforce The Laughs in 2026